Common pre-conceived ideas on Vat exemptions |09 September 2011

First misleading idea – We generally tend to think that an exempt person enjoys an economic advantage because he/she can sell his/her goods or supply his/her services Vat free. We may thus neglect the fact that an exempt person also suffers an economic disadvantage because the Vat paid on his/her purchases is not recoverable or creditable against the Vat he/she would have charged but for the exemption.

Second misleading idea – We also generally tend to think that a Vat exemption (referred to as an “exemption without credit”), reduces the final price of a good or a service. On the contrary, when disrupting the Vat chain a Vat exemption can result in a net increase in total Vat paid through final consumption. If the final retail sale of an item is exempted, the consumer pays no Vat on purchase, but because the retailer cannot take an input credit, the tax paid on its inputs will be embedded in the price paid by the final consumer. The embedded tax, however, is not transparent to the consumer.

Illustration

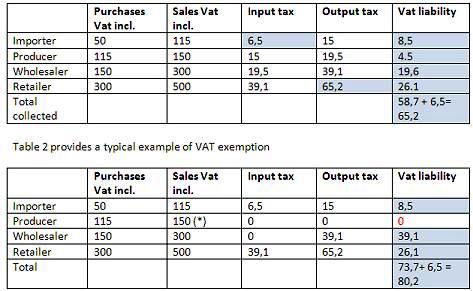

Table 1 provides an example of a Vat chain without exemption.

(*) No VAT is charged

In this example, the producer does not collect Vat and does not receive an input credit for Vat. However, because the wholesaler does not receive credit for any Vat paid, Vat attributable to the importer’s sale is effectively paid twice—once by the importer and again by the wholesaler—causing the total Vat collection to increase as a result of the exemption.

As is evident from table 2, if a sale by an inter-mediate seller is exempt, but the sale by the retailer or the consumer is subject to Vat, there are two effects: the government receives more revenue than it would if there was no exemption (80.2 versus 65.2 in the example) and there is a cascading or pyramiding of the tax when the Vat is applied to those embedded taxes at subsequent stages.

For more information

You can contact Seychelles Revenue Commission on 4293737 or email us at advisory.center@src.gov.sc. The Value Added Tax Act, 2010 is available on the Seychelles Revenue Commission website (www.src.gov.sc)

Submitted by the Seychelles Revenue Commission