2015: Building further resilience against external shocks amid domestic demand pressure and unfavourable external environment |31 December 2015

The initial projection was that Seychelles’ economy would grow by 3.5% in 2015, supported by low and declining global commodity prices, most notably that of oil.

Domestically, such forecast was to be backed by another positive performance of tourism and associated activity. An improved current account position was expected to be one of the main benefits of the lower import prices while the optimistic performance of the services sector was anticipated to contribute to an increase in export earnings.

However, the higher external receipts were partially offset by a weaker euro in international markets even if domestic economic activity remained robust on the whole. By the second half of the year, most indications were that the annual expansion of the Seychelles’ economy would be stronger than initially anticipated and consequently growth in real GDP was revised upwards to 4.3%.

Key to the 2015’ economic outcome was the performance of the tourism sector. By mid-December 2015, the number of tourists to Seychelles had exceeded 250,000 with the actual outcome showing a growth of 19 per cent compared to the same period last year. Despite the benign outlook in the Eurozone and the unfavourable euro/US dollar exchange rate, growth in visitor arrivals from the European continent – supported by the robust French and Italian markets – was by 11 per cent and Europe remained the core market with a contribution of 62 per cent of the total number of visitors. Moreover, important growth in tourist arrivals was also observed from the majority of emerging markets, namely the United Arab Emirates and China.

Notwithstanding the uncertain external conditions, the pick-up in economic activity was also supported by a strong, unprecedented monthly average of 22 per cent year-on-year growth in credit to the private sector during the first half of the year.

As at the end of October 2015, the growth in the outstanding stock of credit to the private sector had fallen to 11.5 per cent compared to corresponding period last year. Nonetheless, such prolonged and strong double digit growth in credit was likely to trigger an increase in demand with the potential to exert pressure on the exchange that would eventually filter into higher domestic prices. Mindful of this, throughout the year, the implemented monetary policy stance of the Central Bank took into consideration such developments in order to ensure that the institution’s price stability objective is not compromised. In terms of interest rates at commercial banks, an overall increase was observed during the year. Compared to the end-2014’s level, the effective lending rate has risen from 12.05% to 12.55% in October 2015 while over the same period the savings rate grew from 2.31% to 2.90%.

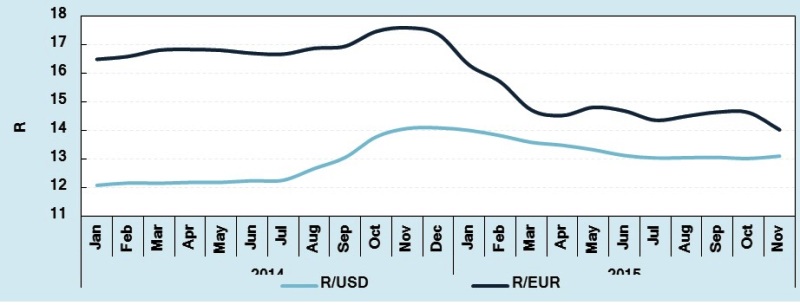

Predominantly as a result of the decline in international commodity prices, the overall demand for foreign exchange remained lower than in the previous year. As at end November, the aggregate reported value of foreign exchange outflows amounted to US $500 million which was 11 per cent less than in the corresponding period of 2014. As for the external value of the domestic currency, this has remained stable at an average of close to R13 against the US dollar for most part of the year after appreciating from a rate of R14 in January.

Chart 01: Exchange rates

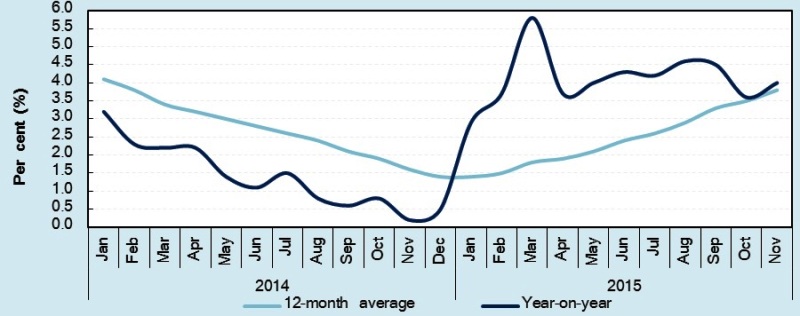

In terms of price development, overall, the consumer price index (CPI) showed relatively higher inflation level in 2015 compared to 2014. Closer analysis of the CPI, reveals that a rebasing of the basket of goods that became effective at the start of the year contributed towards an initial spike in inflation data which later abated. However, seasonal inflationary pressures continued to impact on prices over the course of the year while the stable exchange rate and low energy prices globally contributed towards a moderation in inflationary pressures. In November 2015, the 12-month average inflation rate stood at 3.8% while the year-on-year change in the general price level was 4.0%. The Central Bank expects inflation to peak at the end of 2015 before declining in 2016.

Chart 02: Consumer Price Index

Despite the strong growth in credit, the country’s total value of imports is estimated at less than in the previous year primarily due to the relatively lower commodity prices abroad. This has translated to a narrowing of the country’s current account deficit estimated at 14 per cent of GDP, from 21 per cent of GDP in 2014. Such outcome was also aided by a decline in imports related to foreign direct investment (FDI) as tourism carrying capacity nears saturation point in the economy.

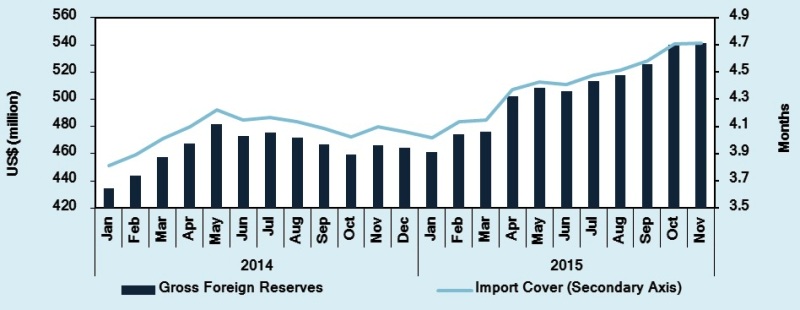

The improved external position was also reflected through an increase in the level of official reserves. Foreign exchange reserves depict an economy’s resilience and its ability to weather external shocks. This is of critical importance for Seychelles given the openness of the economy. Consistently, throughout 2015, the Central Bank has maintained its policy of accumulating reserves whenever such opportunity arose. By mid-December 2015, gross international reserves stood at around US $540 million compared to US $464 million at the end of 2014 resulting in an improvement in reserves adequacy from 4.1 months in 2014 to 4.7 months.

Chart 03: Gross Reserves and Import Cover

On the policy front, the authorities have ensured that the monetary and fiscal policies being implemented are consistent with the prevailing economic environment. In terms of monetary policy, in anticipation of inflationary risks ahead, the Central Bank kept monetary policy tight for most part of 2015 before opting for a cautious loosening in the fourth quarter albeit mindful of local developments and a further weakening of the euro against the US dollar.

In terms of fiscal policy, the government remained on track to record another primary surplus which is estimated at 3.8 per cent of GDP. Total revenue is projected to end the year at 32 per cent of GDP, with value-added tax being the main source of tax income, at 9.2 per cent of GDP. Such fiscal outcome is consistent with the government’s objective of reducing public debt down to 50 per cent of GDP by 2018.

At the end of 2015, the aggregate public debt is projected to stand at 63 per cent of GDP.

Contributed