Financial leasing in Seychelles |18 April 2016

The Central Bank of Seychelles has been working on providing for the enabling environment to allow for the evolution of our financial sector. The introduction of the legislative framework for the licensing and regulation of financial leasing institutions in Seychelles forms a key part of the aim to increase the available financing options.

Accordingly, the Central Bank of Seychelles (CBS) will be issuing a set of three articles aimed at creating awareness on this alternative financing solution which will shortly be available. The first part will aim to introduce the core concept behind financial leasing and contrast it to the more common financing option, which is via loans. The second part, will touch briefly upon the typical process which one would have to go through in applying for a finance lease. The third and final part of this series of articles will in essence outline the benefits of a finance lease for Small and Medium-Sized Entrepreneurs (a segment which stands to benefit immensely from finance leases) and in doing so highlight some of the beneficial elements for the financial leasing institution, which will serve to encourage these to take venture into this segment of the market.

Part 1: Introduction to Financial Leasing (FL) concept

Financial Leasing (FL) is used all over the world and is an alternative means for financing moveable assets. An FL agreement is of a tri-partite nature, meaning that this is an agreement entered into by three parties. More details are provided in respect of these three parties in Table 1.

Table 1: Three parties to an FL agreement

Party Legal definition Explanation

Lessor

A person licensed or approved, to conduct financial leasing business and who transfers the right to possession and use of an asset under lease to a lessee.

This will be the company licensed by the Central Bank in order to offer such a financing option. This could include banks which are granted approval in this regard, as well as other non-banks. Accordingly, businesses will have to apply to these companies in order to request funding for equipment via an FL agreement. One would be able to go to the banks, but also to other companies which are licensed specifically for the purpose of engaging in FL business in Seychelles.

Lessee

A person who acquires a right to possession and use of an asset under the lease for an agreed period of time in exchange for agreed lease payments.

This will be the person applying for financing for the purchase of the asset. These assets will generally be used by the business in order to generate a revenue for the business and to allow for the scheduled repayments to be effected.

Supplier

A person who supplies an asset for the purpose of a financial lease, and transfers title to the asset to the lessor for delivery to the lessee.

This will be the supplier of the asset. The supplier will be paid directly by the lessor and typically will transfer the title of ownership to the asset over to the lessor, but can deliver the asset over to the lessee if so agreed.

An FL agreement can be defined as an agreement between three parties –namely the lessor, lessee and the supplier – whereby the lessor provides an asset for use by the lessee, for a period of time (known as the tenor) in return for specified payments by the lessee.

In Seychelles, the Central Bank of Seychelles expects to commence accepting licence applications from prospective financial leasing institutions (FLI) within the second quarter of 2016. In anticipation of this, the first part of this article is intended to create awareness of the upcoming development and to provide a general insight of FL and to highlight some of the most prominent potential benefits which this new financing option can bring. It will be followed by two more parts, the second of which will touch upon the benefits which FL can bring for SMEs, and the final part providing an illustrative view of the process for applying for an FL.

Currently, when a business wishes to fund a piece of equipment to be used as part of its business operations, one would generally go to a bank to acquire a loan in the absence of available unallocated funds to purchase the asset outright (i.e. payment in cash). With the development of the FL sector, businesses will have a greater choice. Rather than only having the banks to go to, one will be able to shop around and compare the offerings from both banks and FLIs.

It is worth noting that while banks will, subject to the Central Bank of Seychelles approval, also be able to commence offering FLs, it is expected that there will also be other companies which are not banks that may wish to apply for an FL licence. We typically refer to these as non-bank FLIs. Central Bank of Seychelles’ requirements for these will be less demanding in the case of non-deposit-taking FLIs, (as compared with deposit-taking FLIs which will generally be regulated more like banks).

Accordingly, there will be more choice and this choice element will allow the customers to better negotiate and find the best deal for their purpose.

With this point in mind, let us now consider some of the typical aspects of an FL and contrast these to the more common financing options which are used locally, for instance loans.

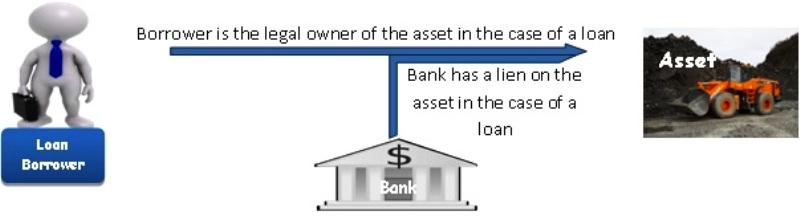

When one applies for a loan, the banks mostly require the applicant to provide a collateral as security for the loan or to provide guarantors, unless it is an unsecured loan, in which case the applicant is typically subjected to higher interest rates to account for the increased risk of such exposures. The collateral or guarantor requirement typically serves as a form of security and provides the bank with a sense of guarantee that the person will repay the borrowed amount and interest, as agreed. Once the loan request is approved, the funds are disbursed to the applicant, who then directly effects payment for the purchase of such asset from the supplier. This asset is owned by the borrower, with the bank having a lien on the asset. Accordingly, the borrower cannot sell the asset without the bank’s approval. Therein lies one of the key distinguishing element between a loan and a FL and this is illustrated diagrammatically in figures 2 and 3.

Figure 1: Diagrammatical illustration of ownership and lien in the case of a loan

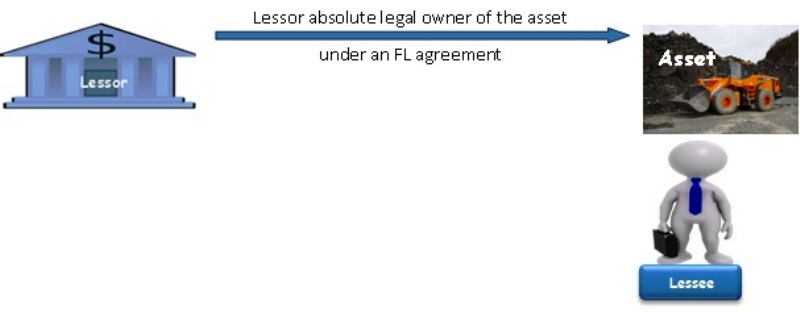

Figure 2: Diagramatic illustration of an fl agreement

Under an FL, the lessor retains legal ownership of the asset, while the lessee is granted the right to possess and use the asset during the tenor, in return for agreed monetary repayments. This is illustrated in figure 2. Accordingly, even if one has the asset in their possession, it is legally registered and owned by the lessor. As such, the asset itself serves as the collateral/security for the financing, as the lessee does not own the asset during the tenor.

In some cases however, particularly involving the financing of specialised assets, the lessor may require a partial contribution towards the cost of the asset, although such will seldom be the case for standard assets (which have a readily available domestic second hand market). For clarity, equipment that will have to be tailor-made or customised for the lessee would effectively be deemed as specialised assets. These will quite probably not be easily re-saleable locally without taking a significant hair-cut in value, i.e. a reduction in its re-sale price. This contrasts to standardised assets.

The right to possess and use the asset by the lessee, subject to the terms and conditions of the FL agreement, allows for the generation of an income for the lessee’s business, while allowing more flexibility in regards to working capital. Optimally, the asset’s use will generate an income in excess of the agreed repayments, thereby allowing the periodic repayments to be effected to the lessor. In fact, a significant part of evaluating an FL application will touch upon the income generation potential that said asset will bring for the lessee. It also allows a business to better manage its finances and free up their cash-flow, allowing such to be more efficiently allocated.

FL is generally more targeted towards large value moveable asset acquisition, principally being acquired for commercial ventures. Thus, for illustrative purposes, assets that could be financed by an FL could include earth moving equipment (such as dump trucks and excavators), cranes, fishing boats, just to cite a few. Tourism establishments wishing to also invest in a large volume of a certain type of asset could also acquire such through an FL, and this could include things such as television units for each room, hairdryers, kitchen equipment and mini-fridges, etcetera. It is also common around the globe for farmers and fisherman to acquire equipment via an FL.

With this point in mind, it is worth noting that under an FL, a common practice is to have greater flexibility. Given that focus is accorded to the income generation potential that the asset will bring for the lessee, FLIs commonly take into account pre-determined patterns and fluctuations in the earnings of the lessee. For instance, in Seychelles, repayment for establishments engaging in tourism-related activities could be structured around the peak and off-peak periods, with higher repayments to be made during peak periods of the year and lower repayments during off-peak periods of the year. This same principle could apply for lessees operating within our fisheries sector. Smaller repayment amounts can be structured during the south east monsoon, when the seas are rough and catch is generally low. The bulk of the repayments could be structured for the north west monsoon when the sector’s performance fares better. In a similar manner, the same principle could apply to the agricultural sector, bearing in mind its own seasonal specificities.