2017: Positive growth in overall output despite a challenged economic environment |29 December 2017

Although the global economic environment remained somewhat uncertain in 2017, the general view by most analysts is that signs of a further strengthening in activity were apparent during the year. Taking into consideration developments in regions with strong economic ties with Seychelles, no major adverse impact has been experienced on the home economy despite its heavy reliance on the rest of the world.

By the end of 2017, the broad structure of the Seychelles’ economy is expected to remain unchanged with services maintaining its status as the key sector in terms of contribution to foreign exchange earnings, GDP as well as employment generation. Most indicators suggest that the economy will record another positive growth in overall output, at a rate estimated at around the same level achieved in 2016. The annual growth in real GDP for 2017 is forecasted at 4.2 per cent.

Key to this outcome is the performance of the tourism sector which has been relatively robust throughout 2017. By December 10, 2017, the number of visitors to Seychelles amounted to 326,523 which was a growth of 16 per cent compared to the same period last year. Consistent with the established trend, most of these visitors – or 62 per cent of the total – originated from Europe. In terms of contribution by country, the main market was Germany followed by France which respectively supplied 15 per cent and 12 per cent of the aggregate visitor arrivals for the above-mentioned period. There was also a notable increase in the number of visitors from emerging markets, particularly the United Arab Emirates. As regard to income generated by the sector, the direct contribution to foreign exchange earnings of the country – in US dollar terms – is expected to increase by at least 5.7 per cent in 2017 from US $414 million estimated in 2016. Notwithstanding this outcome, many stakeholders continue to be of the view that tourism yields need to be maximised such that the sector can enhance its overall contribution to the economy.

While the positive performance of the tourism industry stimulates activity in auxiliary sectors such as transport and telecommunications, a number of segments of the economy reported some challenges. For example, the manufacturing sector has expressed concerns over high operating cost including utilities in addition to facing stiff competition from imported substitutes. Moreover, the resolution to impose a quota on the catch of yellow fin tuna by the Indian Ocean Tuna Commission has brought about some degree of uncertainty to investment in the fisheries sector, particularly in relation to plans to develop the Blue economy.

In the labour market, skill mis-matched as well as relatively low productivity of the local labour force were the main concerns raised. Evident is the increasing number of expatriate employees across more economic segments by contrast to being mainly concentrated in the construction and tourism industries. In terms of unemployment data, the National Bureau of Statistics (NBS) reported a rate of 3.9 per cent in the second quarter of 2017 with a labour participation rate of 70 per cent. For the same period, the unemployment rate for the male population was 3.5 per cent and that for the female population was 4.2 per cent.

While the increase in employment of foreign labour is deemed required in some sectors of the economy, it also implies higher leakages to the rest of the world. This is primarily in the form of remittances destined to the country of origin of the expatriate worker and therefore represents additional demand for foreign exchange that is generated by the country.

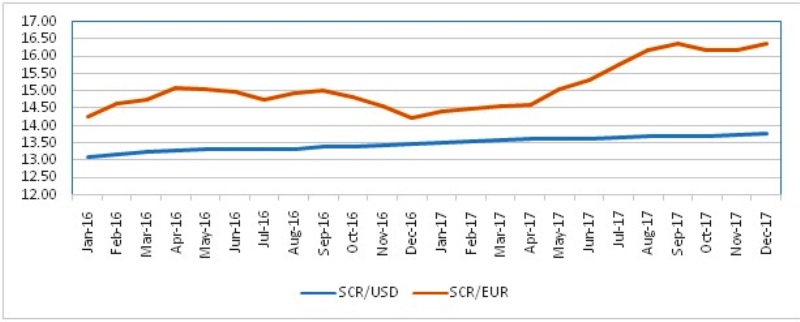

Statistics on foreign exchange transactions show that by mid-2017, inflows of foreign exchange into the domestic economy has increased compared to the same period of 2016. Such outcome is consistent with the reported growth in visitor arrivals. Over the same period, growth in demand has also been recorded. While international dynamics would influence the external value of the rupee, the forces of domestic demand and supply continued to be key. Overall, the rupee has weakened against its main trading partners during 2017, particularly in comparison to the US dollar and euro.

Chart 01: Exchange Rates(SCR per currency, period average)

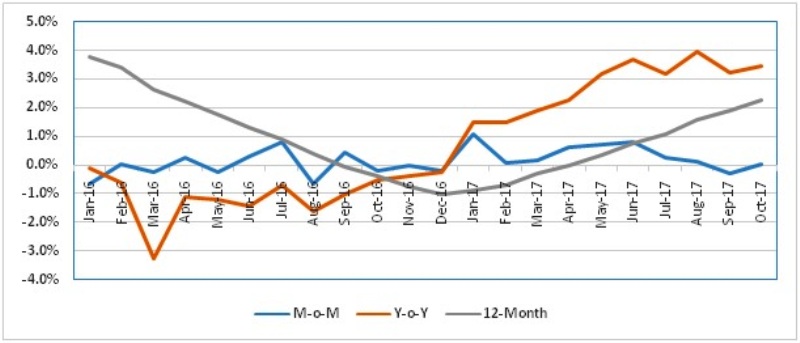

Consistent with the depreciated domestic currency, inflationary pressures have peaked up in 2017 and as can be seen on Chart 02 – based on the consumer price index statistics published by NBS – the rate of increase in prices has been stronger than in the previous year. In addition to the second round effects of the weakened domestic currency, the pick-up in inflationary pressures has also been influenced by the revision in excise on fuel, tobacco and alcohol that came into effect in May.

Chart 02: Consumer Price Index (Measures of Inflation)

Notwithstanding the observed higher general price level in 2017 compared to 2016, the Central Bank is of the view that inflation will be at a modest rate and will not pose a threat to domestic price stability. As a result, the monetary policy stance has been relaxed since the second half of the year in order to provide a boost to economic activity given indications of existing scope to enhance activity level across the economy.

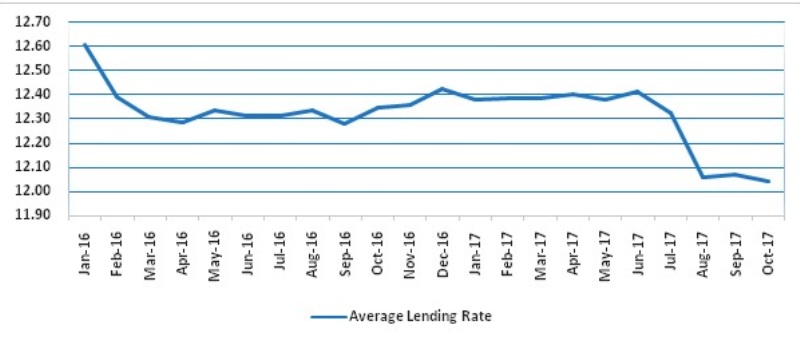

Following such decision, an overall reduction in interest rates has been observed. The effective average lending rate fell from the year’s peak of 12.41 per cent in June to 12.04 per cent in October which was also lower than 12.35 per cent observed in October 2016. Compared to June 2017, the average return on fixed-term rupee deposits has fallen from 3.86 per cent to 3.55 per cent in October while the savings rate declined from 3.06 per cent to 2.37 per cent over the same period. Consistently, the yield on Treasury bills has also declined, with that on 91-day maturity falling from 5.04 per cent in June 2017 to 2.75 per cent in October 2017.

Chart 03: Average Lending Rates (in per cent per annum)

Expectedly, a growth in the aggregate demand for loans has been observed. At the end of October 2017, the total stock of outstanding credit from lending institutions disbursed to the private sector has increased to R5,868 million, by 14.5 per cent compared to December 2016 or by 15.2 per cent in relation to October 2016. Most of these loans went towards the financing of consumptions. At the end of October 2017, the share of credit allocated to private households was 22 per cent of the total outstanding amount.

Given the nature of the Seychelles economy, the majority of these loans represent demand for imported goods or services. This stated, provisional forecast show a slight improvement in the country’s current account deficit for 2017 to 16 per cent of GDP from 18 per cent of GDP the previous year, predominantly due to improved export earnings, particularly services. The country’s insurance against external shocks also improved in 2017 as measured by the increased level of international reserves. From US $523 million at the end of 2016, gross official reserves rose to US $556 million at the end of November 2017, which is equivalent to about 4 months of the forecasted total value of the country’s imports of goods and services.

In June, the 3-year programme arrangement with the International Monetary Fund (IMF) under the Extended Fund Facility (EFF) came to an end. This was the completion of the third IMF financing programme by Seychelles since 2008 under which the country has been able to restore macroeconomic stability, reduce public debt to a more sustainable level and implement significant reforms among other achievements. Nevertheless, as a small island developing state, Seychelles remains vulnerable to external shocks and further reforms that are structural in nature remain the key focus going forward. Hence, the authorities have found it important to continue engagement with the IMF to benefit from the oversight, discipline and advice from the IMF. As such, following completion of the EFF, negotiations started for a new programme, namely a three-year Policy Coordination Instrument (PCI) that was subsequently approved by the Executive Board of the IMF at its meeting of December 13, 2017. The PCI is a new instrument designed to help countries in the formulation and implementation of policy packages with close monitoring of progress by the IMF. In contrast to the previous programmes, the PCI is without financing support.

During 2017, the government remains committed to fiscal discipline and reduction of public debt to a more sustainable level. Fiscal policies is focused on achieving a primary surplus which should finish 2017 at 3.0 per cent of GDP and not anticipated to reach below 2.5 per cent of GDP in the subsequent years. As for total public debt which is expected to end 2017 at 67 per cent of GDP, this is targeted to fall to below 50% of GDP by 2020.

Looking ahead, the Seychelles economy remains vulnerable to external shocks and therefore susceptible to developments from across the globe. Tourism is to maintain its position as the key sector of the economy and the expected increase in air access to important markets should provide a further boost to the sector. Therefore, the contribution of the services sector to the Seychelles’ economy is anticipated to remain positive in the coming year which should continue to support activity in auxiliary sectors despite indications that the national airline would face new challenges which will warrant a change in strategy in order to remain financially viable. The latest indicators suggest no imminent strong risks of imported inflationary pressures emanating from international commodity markets although some upticks in some prices are anticipated. From a domestic perspective, inflationary impulses is likely to originate from the second round effect of the depreciated domestic currency and revision in administrative prices such as that of utilities. It is likely that challenges being faced by businesses in terms of high operating cost and tough competitions from imported substitutes will continue to prevail in 2018. The level of international reserves is forecasted to remain around four months of the country’s import requirements which according to a number of measures is deem “adequate” to cushion the country against a fair degree of external shocks. Overall, the economy is forecasted to achieve another positive growth in output but at a reduced pace of 3.3 per cent in 2018 compared to 4.2 per cent in 2017.