Annual review of the Seychelles’ economy-Tourism remains key foreign exchange earner |30 December 2011

While such expansion in economic activity is at a reduced pace compared to 6.7% estimated for the year 2010, it represents a positive outcome given the overall uncertainty and pessimistic outlook surrounding the global economic environment. Hence, despite Seychelles’ openness and thus its high dependency on global economic conditions and consequently vulnerability to external shocks, such performance indicates that domestic economic activity has during 2011 shown some degree of resilience.

Tourism remained one of the key sectors in terms of its contribution to foreign exchange inflows, employment as well as GDP. All indications are that the year 2011 will register a new record number of visitors to the country; at least 10% higher than 174,529 tourists reached in 2010. Europe continues to supply the majority of visitors to the Seychelles despite the uncertainty relating to the financial crisis in the Eurozone. In terms of direct earnings from tourism and related activities, the estimate for 2011 is US $298 million compared to US $274 million in the previous year.

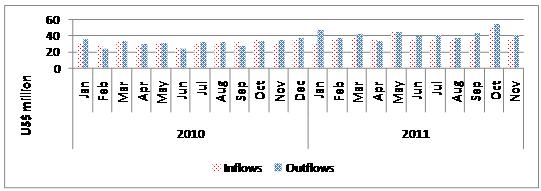

Total gross foreign exchange inflows into the system reported by authorised dealers (commercial banks and bureau de change), for the period January to November 2011 amounted to US $419 million, representing an increase of 24 per cent compared to the same period in 2010. However, the demand for foreign exchange has risen at a much higher pace than the growth in supply (see chart 01). At a cumulative total of US $469 million recorded for the eleven months to November 2011, the rise in the demand met by authorised dealers was an increase of 36 per cent compared to the same period in the previous year.

Chart 01: Foreign exchange transactions

Despite a dynamic foreign exchange market throughout the year, the strong demand for foreign exchange, coupled with the depreciation of the euro against the US dollar in the international markets have contributed towards the overall depreciation of the domestic currency. The latter relates to the fact that foreign exchange earnings are predominantly in euro whilst payments are in US dollar which implies the euro/US dollar cross rate plays an important role in influencing domestic exchange rates. By December 28, 2011, the Seychelles rupee has weakened to an average of R13.57 per US dollar and R17.75 relative to the euro compared to R12.15 and R16.13 end-December 2010, respectively.

During the year, the economy was also affected by changes in world commodity prices. Given the openness of the Seychelles economy, the country was highly exposed to imported inflationary pressures. This was primarily related to the rise in international commodity prices including food and oil, the pass-through of which resulted in an increase in the general price level domestically. Notable is the price of oil which not only impacted the cost of fuel consumed directly such as in motor vehicles but also that of utilities following revisions in tariffs by the Public Utilities Corporation (PUC) to cater for elevated costs of production.

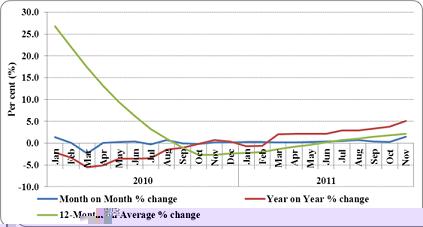

As such, given the high import content of domestic consumption, inflationary pressures were mainly driven by external factors. Measured based on changes in the Consumer Price Index (CPI) compiled by the National Bureau of Statistics (NBS), year-on-year inflation for November 2011 stood at 5.1% against 0.4% recorded in December 2010 (see chart 02).

Chart 02: Inflation

Consistent with the overall higher level of activity, the year 2011 observed a growth in credit extended by commercial banks. Compared to December 2010, credit to the private sector increased by 6.6% in November 2011. Growth was also registered in the total value of imports which has resulted in a widening of the current account deficit to above the 23% of GDP mark estimated for the year 2010. Of note is that a significant proportion of this import represents commodities that are required for the implementation of new investments. For the year 2011, total gross inflow of foreign direct investment (FDI) is estimated at US $128 million, the majority of which are hotel projects.

Despite the worsened current account position, the Central Bank continued to accumulate external reserves as per one of the performance criteria set out under the on-going macroeconomic programme started in November 2008. The year 2011 is expected to end with gross official reserves of US $268 million equivalent to 2.4 months of import compared to US $254 million end-December 2010.

On the fiscal front, the government continued to record positive results. Given better-than-anticipated collection of revenue and the containment of expenditure, the budget outcome for the year 2011 is expected to record a primary surplus of at least 4.5% of GDP. The positive fiscal outcome has also allowed the government to reduce public debt further. The total stock of public debt is expected to end the year 2011 at around US $800 million or equivalent of 79% of GDP of which 50% of GDP represents external debt. At the end of December 2010, total public debt stood at 83% of GDP.

Contributed